FAQs on funding for lending programmes

The Riksbank decided to terminate this programme on 20 September 2021. The last auction procedure of the programme was held on 10 September 2021. In this programme, the Riksbank offered funding to banks of up to SEK 500 billion against collateral to stimulate their lending to companies operating in Sweden. In this way, the Riksbank helped companies to meet the financial challenges resulting from the pandemic.

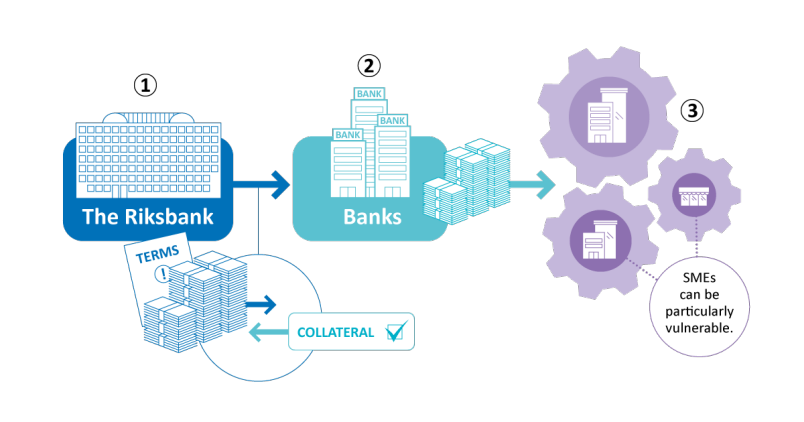

How the Riksbank’s funding for lending worked

1. The Riksbank offered loans to banks against collateral at an interest rate set at the policy rate. The aim was to facilitate banks’ lending to non-financial corporations, including sole proprietors.

2. If banks did not increase their lending to these companies, they had to pay additional interest to the Riksbank.

3. Companies could apply to banks for loans, which might alleviate the financial challenges caused by the coronavirus pandemic.

Did the Riksbank lend money directly to companies?

The Riksbank lent money to banks, i.e. our monetary policy counterparties. Banks could then lend money to companies.

Why didn’t the Riksbank lend money directly to companies?

The Sveriges Riksbank Act (1988:1385) stipulates the Riksbank’s mandate, which is decided on by the Swedish Parliament, the Riksdag. According to the Act, the Riksbank must receive “adequate collateral” when it lends money. This is because the Riksbank is an authority and must not take excessive financial risks.

The Riksbank functions as the banks’ bank. Put simply, this means that, when necessary, we provide banks with money at a particular interest rate and these funds can then be passed on into society as loans. Therefore, banks themselves decide which companies can receive loans, and at what interest rate. Riksbank can influence banks’ willingness to lend money, but not force them to do so.

In times of crisis, direct government support to companies may be necessary, for instance, credit guarantees and reduced taxes and charges. Such decisions are made by the Riksdag and the Government within the scope of fiscal policy, and not by the Riksbank, which is responsible for monetary policy.

How much interest will companies have to pay to banks?

Banks pay the equivalent of the repo rate, which is currently zero, on loans from the Riksbank. It is then up to the banks themselves to determine what interest rate companies will pay. The interest rate banks charge to companies is based on what banks pay for the money and what supplement they add on. However, the Riksbank's decision means that banks’ cost for the money is currently zero.

Do banks decide who has the right to the loans and what does this process look like?

The Riksbank’s decision means that banks are offered an interest rate equivalent to the repo rate, which is currently at zero per cent, on loans from the Riksbank, if they can later prove that they have passed the money on to companies. If a bank does not increase its lending to companies, it must pay a slightly higher interest rate to the Riksbank. It is therefore the individual bank that ultimately determines exactly which companies will have access to the current loans.

Why didn’t banks lend more of the money that the Riksbank was prepared to provide to them?

Whom it lends to is ultimately the bank’s decision. The Riksbank’s role was to ensure that there was liquidity in the market so that solvent companies did not need to go bankrupt due to a lack of liquidity.

Where did the SEK 500 billion come from?

The Riksbank can create money not only by issuing banknotes and coins but also by issuing electronic money in Swedish kronor (SEK) to banks, and this is what the Riksbank did.

When the Riksbank lends money to banks, a debt to the general public is created but at the same time, the Riksbank receives assets, such as government securities and other bonds, from banks as collateral. This increases the Riksbank’s balance sheet.

A central bank cannot just create money as it likes. If too much money is created, it may lead to rising prices (inflation), but if too little is created, it may instead lead to falling prices and lower activity in the economy.

How is it ensured that only “robust” companies receive subsidised loans?

Ultimately, the individual bank decides which companies it will lend to. The Riksbank is not able to, and should not be able to, determine this. The purpose of the measure was to bridge over a potential shortage of money in the banking system that could have become a problem during a difficult period for companies that were robust prior to the current crisis and could be expected to be robust again when the economy returned to normal.

Who bears the counterparty risk in the money lent?

Banks take the counterparty risk.

Does the Riksbank set requirements as to how companies may use the loans?

No, the Riksbank does not set any requirements for how companies may use these loans. The Riksbank only sets the requirement that banks must use the money to increase their lending to companies.

Why doesn't the state/the Riksbank bear the risks for the loans?

The Riksbank bears the risk for the loans to banks (the Riksbank’s customers) but it is up to banks to make credit risk assessments of their customers. The Riksbank has eased the requirements for collateral that we normally impose on loans to banks. This means that the Riksbank is taking on some of the risk in these loans. The Government has also established a corporate loan guarantee programme, a kind of “corporate ER”. Through this guarantee programme, the state takes on most of the risk associated with lending to companies that are being hit financially by the coronavirus but are otherwise viable. The National Debt Office offers the guarantee to credit institutions that in turn issue guaranteed loans to companies. Read more about the corporate loan guarantee programme on the National Debt Office website.

What did the decision to include lending to sole proprietors mean?

There are a number of companies run as sole proprietorships that are not categorised as non-financial corporations in the statistics and were therefore not originally included in the programme. In a sole proprietorship, the company and its owner are the same legal entity. The company’s corporate registration number is the same as the owner’s personal identity number. These are referred to in the statistics as entrepreneurial households. The Riksbank decided on 6 April 2020 to extend the programme so that lending to sole proprietors was equated with lending to other non-financial corporations. As before, however, the bank itself decides which companies can access the loans.

Were there two different lending programmes?

Yes, there were two different programmes. The programme launched in March 2020 had terms that were not suitable for long-term application. In March 2021, the Riksbank therefore decided to launch a revised programme. That programme was then terminated in September 2021. The basic aim of the two programmes was the same, to support banks’ lending to non-financial corporations. Some details differed, such as the maturity periods for the loans and the method for evaluating the banks’ lending to companies. Loans from the Riksbank are still available to banks under the old programme, but not the new programme.

Thanks for your feedback!

Your comment could not be sent, please try again later

Questions? Visit our FAQ on kundo.se (opens i new window).