Market divided on functioning of fixed-income market

News The Riksbank's Financial market survey shows that the number of market participants who consider the fixed-income market to be functioning well is the around the same as the number who consider it is functioning poorly. A shortage of liquidity is cited as the most common reason for poor functionality and one reason given for this is the Riksbank's purchases of government bonds. A severe decline in prices of housing and property in Sweden is regarded as the largest risk to the Swedish financial system.

The number of participants who consider the fixed-income market to be functioning well or very well is around the same as the number who consider it to be functioning poorly or very poorly. A majority of the latter state limited or poor liquidity as the main reason for the poor functionality of the fixed-income market and several mention the Riksbank's government bond purchases as one of the reasons. Many also consider that a possible normalisation of the Riksbank's expansionary monetary policy, with repo rate increases and quantitative tightening can improve the market functioning over the coming six months.

Housing and property market – primary risk

Market participants see a severe deterioration in the housing and property market in Sweden as the primary risk factor for the Swedish financial system. When asked to list events that risk having a negative effect on the financial system, the respondents name credit and liquidity risks, market risks from, for instance, Brexit, and increased regulation.

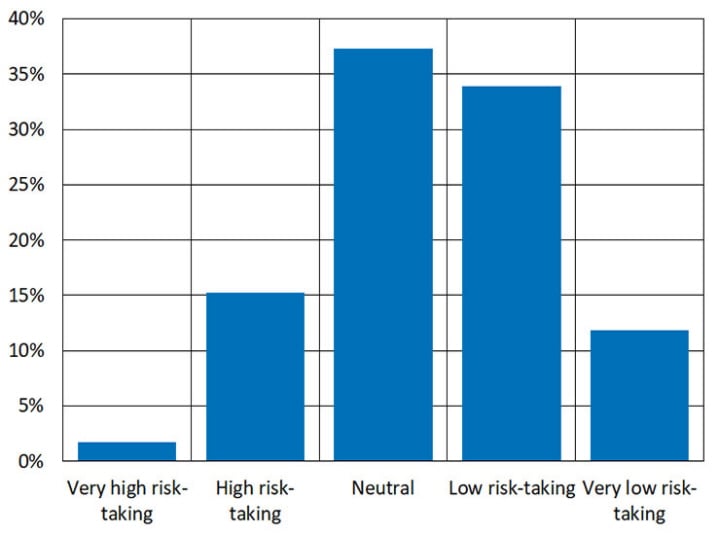

The majority of respondents describe their risk taking as low or neutral

Most of the market participants describe their general risk taking on the market as low or neutral, and only a few participants consider their general risk taking to be high or very high. A clear majority of the respondents consider they have reduced their risk taking or say they have the same level of risks as before. Most consider that they are in general well prepared to deal with potential risks, such as credit and counterparty risks, market risks, liquidity risks and legal risks. One in six respondents say they are poorly prepared for cyber risks.

Diagram: In general, what is your assessment of the functioning of the Swedish fixed-income market today?

With effect from autumn 2018, the Riksbank will send out at regular intervals a questionnaire (the Financial markets survey) to participants active in the Swedish fixed-income and foreign exchange markets. The purpose of the survey is to gain an overall picture of the participants' views on the functioning of the Swedish financial markets, market activity and what risks they see in the Swedish financial system going forward. Compared with the earlier Risk Survey, the Financial market survey is based on an updated questionnaire that covers functionality, market activity, risks, risk taking and other overall questions with regard to both the fixed-income and foreign exchange markets. This report describes the results of the survey where responses were received between 6 and 16 November 2018. The survey was sent out to 99 participants, both Swedish and non-Swedish, who are active in the Swedish fixed-income and foreign exchange markets. The response rate was 56 per cent. The report is based solely on the participants' responses and does not reflect the Riksbank's assessments.