Stablecoins are intended to maintain a stable price over time

Published: 19 May 2022

How do stablecoins differ from other cryptoassets?

Stablecoins are a kind of cryptoasset that are intended to maintain a stable value over time, for instance by tracking the price of a national currency such as the US dollar.[43] For a more comprehensive overview of the structure of different types of stablecoins, see D. Bullmann et al. (2019), “In search for stability in crypto-assets: are stablecoins the solution?”, Occasional Paper Series, No. 230, European Central Bank. They therefore differ from many other cryptoassets, which do not have stabilisation mechanisms. Instead, their values fluctuate freely.

The value of stablecoins is generally backed by a reserve that can consist of different assets and they can thus be called collateralised stablecoins. The collateral can be financial assets such as commercial paper, bank deposits in one or several national currencies or even other cryptoassets.

There are also algorithmic stablecoins, also called non-collateralised stablecoins, which do not have a reserve of assets that fully equals the value of the issued coins. Instead, an algorithm adjusts the price based on supply and demand, keeping a stable level over time. In short, when the price rises, new stablecoins are created to increase the number of stablecoins in circulation, which has the purpose of reducing the price. When the price falls, the number of stablecoins is reduced – they are repurchased and destroyed. This process can be more or less automated. For example, it might be that part of the process, such as the creation and destruction of coins, is not automated.

Stablecoins can also be a combination of the versions described above, for instance a collateralised stablecoin but with certain features from algorithmic stablecoins. This staff memo focuses mainly on collateralised stablecoins.

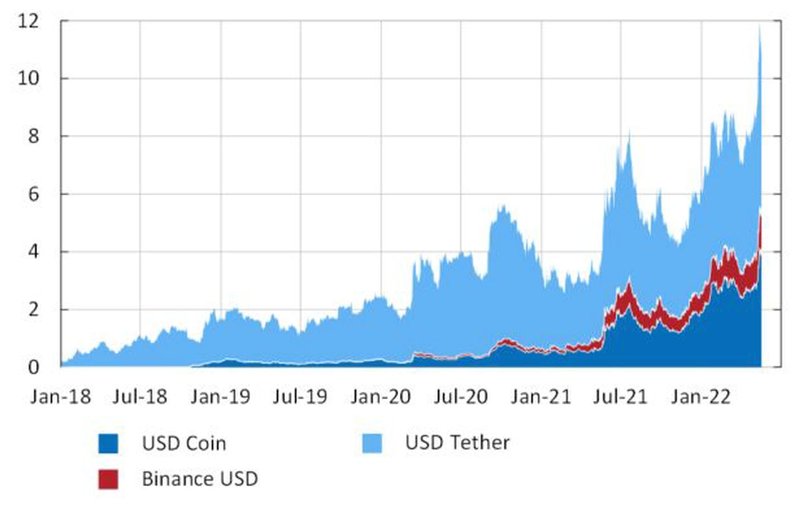

Three of the largest stablecoins that exist today – USD Tether (USDT), USD Coin (USDC) and Binance USD (BUSD) – are intended to maintain a 1-to-1 relationship with the US dollar. These are examples of collateralised stablecoins.

Like other cryptoassets, stablecoins too have grown in popularity in the past few years, resulting in growth in their market value. They now make up a sizeable share of the total market for cryptoassets. The market value of USDT, USDC and BUSD currently equals approximately one tenth of the total market value of cryptoassets (see Figure 5). Unlike other cryptoassets like Bitcoin and Ethereum, the increase in market value is not due to price increases, but to an increase in the number of issued stablecoins. This also means that the asset reserves for these stablecoins have increased in size.

The overall market value of euro-pegged stablecoins, including EUR Tether, is relatively low thus far. There is currently no major stablecoin pegged to the Swedish krona.

Many stablecoins are available for anyone to buy at various trading venues and can be kept in crypto wallets. There are however examples of stablecoins which, at least for now, are only intended for institutional investors. One is JP Morgan’s JPM Coin, which is fixed at 1 to 1 to the US dollar. JPM Coin is used for immediate payments between accounts at JP Morgan.[44] E. Mitchell (2021), “What is JPM Coin and How Do You Buy It?”, 10 January 2021, Bitcoin Market Journal.

The term ‘stablecoins’ might be misleading

In order for the value of stablecoins to be stable, it is essential that the assets backing them are liquid and stable in value. Another condition is that the size of the reserve must equal issued stable coins; that is, when new stablecoins are created, new reserve assets must increase correspondingly. When stablecoin holders instead redeem their stablecoins, these must be destroyed and the reserve assets be reduced correspondingly.[45] FSB (2022), “Assessment of Risks to Financial Stability from Crypto-Assets”, February 2022, Financial Stability Board.

The largest stablecoin, USD Tether, has a reserve that largely consists of short-maturity assets such as commercial paper (see Figure 6). Commercial paper is a type of unsecured asset that could lose value. It could mean that the assets in the reserve no longer suffice to equal issued stablecoins. In that case, they cannot thus be redeemed at the value expected by holders.

The company behind the stablecoin USD Tether was ordered to pay a fine of USD 41 million by an American authority in the autumn of 2021, due to their claim that Tether had been fully backed by assets in traditional currency.[46] CFTC (2021), “CFTC Orders Tether and Bitfinex to Pay Fines Totaling $42.5 Million”, Release Number 8450-21, 15 October 2021, Commodity Futures Trading Commission. It emerged, however, that the reserve assets had not always equalled the number of issued stablecoins and that the reserve included various types of unsecured receivables. Also, the reserve assets had been partly held with unregulated entities or in other jurisdictions and not been subject to regular review. On the whole, these factors could have lead to inability for Tether holders to redeem their stablecoins at the intended value of one dollar.

As the reserve for stablecoins often consists of more traditional financial assets, such as bank deposits or various kinds of financial assets, this also tightens the connection between stablecoins and the financial system as a whole. If a situation emerges in which numerous stablecoin holders want to exchange their stablecoins at the same time for national currency, for instance because they have lost confidence in the stablecoin maintaining its value, the assets in the reserve might need to be sold off or redeemed rapidly. This could in turn cause shocks, such as price corrections, on the markets where the reserve assets are invested and problems for the entities that issue the assets.

There are examples of times when stablecoins have not lived up to their designation. During May 2022, holders of a relatively large algorithmic stablecoin, TerraUSD, sold large volumes during a few days’ time.[47] R. Nieva (2022) and A. Sethi (2022), “Why Crypto Cratered: 5 Things You Need To Know”, 14 May 2022, BuzzFeed News. Different factors are believed to have caused this, but altogether this resulted in the algorithm not being able to uphold TerraUSD’s promised value of one dollar. Instead, the price of TerraUSD collapsed, to circa 15 cent at the lowest on May 13. In conjunction with the drop in TerraUSD, also other stablecoins were affected, also those who are not algorithmic. One example is USD Tether, which dropped by around five per cent at most from the promised value of one dollar and also met demands for redemption from holders. However, the price of USD Tether has thereafter approached one dollar again. Other cryptoassets were also affected by the events. An earlier example of an unstable stablecoin is the case of the small stablecoin, IRON, which dropped rapidly in price during 2021. This was because IRON’s reserve consisted of around a quarter of another cryptoasset, which saw its value drop to zero. At that time, the price of IRON dropped from a value of around USD 1 to 75 cents in the space of a couple of days.[48] The Crypto Ecosystem and Financial Stability Challenges. Chapter in the Global Financial Stability Report, October 2021, International Monetary Fund. Because IRON was a relatively small stablecoin, the drop in price did not have any major implications.

Altogether, these cases illustrate that stablecoins not necessarily are stable. It also shows that it may be difficult to maintain a stable price for a stablecoin if the value of the assets in the reserve is unstable or if their value do not fully correspond to the number of issued stablecoins.

The larger a stablecoin and its asset reserve, the more pronounced the risks. For stablecoins held and used by people worldwide – global stablecoins – the risks could have particularly heavy consequences for both stablecoin holders and the rest of the financial system, because they can spread throughout different economies.[49] G7 Working Group on Stablecoins (2019), “Investigating the impact of global stablecoins”, October 2019, Group of Seven, International Monetary Fund and Bank for International Settlements.