Q&A - The Riksbank's income statement and balance sheet

The Riksbank's equity and the submission to the Riksdag

The Riksbank asked for a 44 billion injection of capital but you are only getting 25 billion, are you happy with that?

The Riksbank has submitted a request to the Riksdag to restore the bank's equity to the statutory base level. This would mean a capital injection of SEK 43.7 billion. As an alternative, we proposed to split the restoration over two years, with 25 billion in a first step. The capital injection of SEK 25 billion now decided by the Riksdag means that our equity (which at the end of 2023/beginning of 2024 was SEK -2 billion) amounts to SEK 23 billion before the result for 2024 is taken into account.

In connection with the decision on the capital injection, the Riksdag stated that it is important that the Riksbank has adequate self-financing. In addition, the Riksdag sent an instruction to the Government to return to the Riksdag with legislative proposals that fulfil the Riksbank's need to strengthen its capacity for self-financing. Such a bill is now on the table and has just gone out for consultation. We need to analyse the details of the bill to assess the whole from the perspective of the requirement for the Riksbank to have sufficient self-financing.

How does the loss in 2022 affect the Riksbank’s equity?

Changes in value in the form of realised gains and losses and unrealised losses leading to write-downs are included in the Riksbank’s reported result. Equity decreases when the Riksdag (the Swedish parliament) adopts the Riksbank’s annual report and approves the allocation of reported loss (or, in normal cases, profit). If the Riksbank instead reports a profit, this approval from the Riksdag covers the proposed dividend to the state. The Riksdag deals with the approval of this allocation of profit in May of each year.

How can the Riksbank rebuild its equity?

In principle, there are two ways in which the Riksbank can rebuild its equity: by making profits or by receiving a capital injection. As the current loss is due to unrealised value losses in the bond holdings, there is a possibility than market rates will fall and the losses decrease again before the bonds mature or are sold. If the Riksbank were then to start making profits again, they could be used to strengthen its equity instead of distributing the profit to the state. Another alternative is for the state to give the Riksbank a capital injection.

Why have you requested a capital injection to the statutory base level stipulated in the Sveriges Riksbank Act, i.e. a contribution of SEK 43.7 billion?

According to the Sveriges Riksbank Act, equity must be restored to the base level unless the Riksbank has unrealised gains in revaluation accounts that can justify a smaller amount. Our assessment is that this is not the case. Given the risks we now face, the unrealised gains we currently have are not large enough to justify restoring our equity to a level lower than the base level. The proposal to request restoration to the statutory base level entails a capital contribution of SEK 43.7 billion in 2024 (read more about the framework for the Riksbank's equity in the new Riksbank Act).

You have very low equity, is a capital injection to the base level sufficient?

According to the Riksbank Act, the submission shall be for an amount that restores equity to the base level, unless unrealised gains on the balance sheet justify a restoration to a lower level or no restoration at all. The starting point is therefore that the submission shall refer to the base level. If required to safeguard the Riksbank’s ability to be self-financing in the long term, the submission may correspond, at most, to an amount that restores equity to the target level.

The Riksbank concluded that the submission should refer to the base level. The buffers in terms of unrealised gains that the Riksbank currently has provide some protection against an even further fall in the Riksbank's equity in the near future. In addition, a quarter of the foreign currency reserves are hedged. Together, this provide some protection if the krona were to strengthen, reducing the value of our foreign currency reserves in kronor. At the same time, our holdings of Swedish bonds will continue to decline going forward and the remaining maturity of the holdings will decrease. This means that the interest rate risk is decreasing rapidly, i.e. the risk of the Riksbank making a new loss if interest rates were to rise again is steadily decreasing. With a restoration of equity to the base level, the Riksbank’s financial position will improve going forward, albeit at a very slow pace. We are also exploring ways to strengthen the Riksbank's self-financing in other ways.

How have you assessed and considered the revaluation accounts when arriving at the capital injection you now propose?

At present, the Riksbank's financial position is heavily influenced by interest rate and exchange rate fluctuations. This includes the buffers in the revaluation accounts, which can change significantly in a short period of time. The Riksbank’s current buffers of unrealised gains provide some protection against a further fall in the Riksbank's equity in the near future. Our overall assessment is that the unrealised gains in the revaluation accounts are insufficient to justify a submission to restore the Riksbank's equity to a lower level than the base level. However, neither is it justified for the submission to be for a restoration to a higher level than the base level at present.

In the submission you mention as an option to split the payment, SEK 25 billion now and the rest next year. Why have you included this option?

The Riksbank's balance sheet is now shrinking rapidly but remains large. Even if equity is restored to the statutory base level in 2024, this year’s result will be very sensitive to interest rate and exchange rate developments. There is therefore a risk that new losses will arise and cause the Riksbank's equity to fall below the base level again as early as at the beginning of 2025. To mitigate these risks, one option is to divide the restoration over two years so that the Riksbank's equity is restored in 2025 to the base level applicable then. This would provide a more solid foundation for the Riksbank to build up equity to the target level in the long term.

Why might the Riksbank need better earnings?

The starting point for the size of equity is that the Riksbank is to be financially independent. Financial independence can be achieved by the Riksbank financing its own administrative costs independently and sustainably.

Financial independence is achieved primarily through the Riksbank’s net interest income, that is the difference between interest income and interest expenses, covering administrative costs and creating scope for financial risk provisions. The Riksbank can achieve positive net interest income by having access to interest-free debt, meaning sources of financing on which the bank does not pay interest. This includes equity and banknotes and coins in circulation.

At the moment, the situation is such that the Riksbank’s balance sheet is still large from a historical perspective, while the Riksbank has a historically small proportion of interest-free debt. This is weakening net interest income and making it more difficult for the Riksbank to be self-financed. The Riksbank is therefore reviewing the possible measures it could take to improve the Riksbank’s self-financing in the long term.

You say that you will investigate long-term earnings. What alternative sources of income are available?

The Riksbank's self-sufficiency depends on both costs and income. We are now looking at ways to reduce costs and increase income. This may include, for example, changes to the management of the foreign reserves and our fees. In this work, the Riksbank needs to investigate the legal, operational and financial aspects of both changes to existing operations and possible new measures. However, it is still too early to say what the results and proposals will be.

How much do you think you need to raise through new sources of income to maintain ample equity over time?

The Riksbank assesses that a restoration to the base level is sufficient in combination with the buffers we have in revaluation accounts and the fact that our financial position will be significantly less sensitive to new interest rate increases. In the long term, we need to strengthen our self-sufficiency, but it is difficult to say exactly how much. What is required for the Riksbank to be self-sufficient will vary over time depending on policy needs and developments in the Riksbank's balance sheet and administrative costs.

When do you expect to finalise the study on new sources of income?

The aim is to provide at least preliminary information during the year. But the issue is complex and involves legal, operational as well as economic aspects.

Why can the Riksbank not ensure financial independence by using the seignorage from currency in circulation?

Most other countries have a large and growing currency in circulation that allows the interest-free capital to generate sufficient returns even if equity decreases. Sweden, on the other hand, have a small amount of currency in circulation, which has decreased as a proportion of GDP in recent decades due to a reduced demand for cash (read more about cash and payments in the Payments Report). The currency in circulation has also fallen as a proportion of the balance sheet, resulting in seignorage having made an increasingly smaller contribution to the Riksbank’s financial result over a long period of time. This means that, unlike other central banks that have made large losses, it is more difficult for the Riksbank to restore its own capital over time and under its own steam by means of a large seignorage.

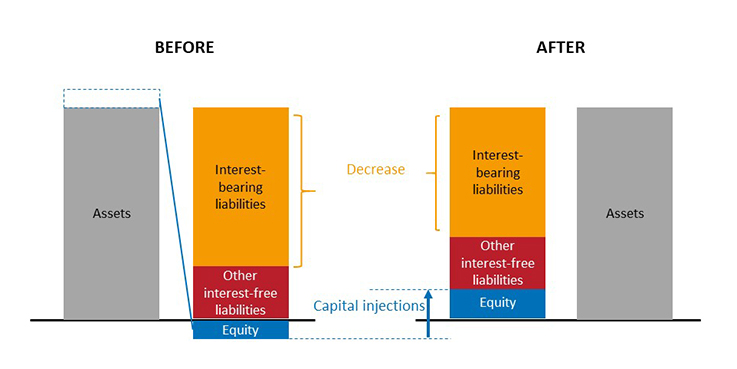

What happens on the Riksbank’s balance sheet when the bank receives a capital injection?

That depends on how the recapitalisation takes place. If the state finances the capital injection by borrowing the money needed by issuing government bonds, the Riksbank’s balance sheet remains unchanged in size. This is because monetary policy deposits (the banks’ overall claim on the Riksbank which is a liability on the Riksbank´s balance sheet) decreases, while the Riksbank’s equity increases to the same extent.

If, for the sake of simplicity, we assume that everything happens in one day, it would look like this: In step 1, when the Swedish National Debt Office issues bonds and the bond buyers (the banks) pay the National Debt Office for the bonds, the banks’ balance of central bank money in the RIX system decreases, while the National Debt Office’s balance of central bank money increases by the same amount. In step 2, the National Debt Office transfers the funds from the bond issue to the Riksbank by crediting its account in the RIX system, which is thereby reset to zero. In this way, the capital injection reaches the Riksbank and the total amount of central bank reserves in the system decreases, which is the same as a reduction in monetary policy deposits.

On the Riksbank’s balance sheet, shown in simplified form in the picture below, this becomes visible when equity grows and shifts from negative to positive at the same time as monetary policy (interest-bearing) deposits shrinks. Overall, the size of the balance sheet does not change but there is a redistribution between interest-bearing monetary policy deposits and interest-free debt (equity).

About the Riksbank’s loss

The Riksbank made a loss of SEK 81 billion for 2022. What is the reason for this large loss?

It is due to a large reduction in the value of the Riksbank’s bond holdings when interest rates rose in 2022.

Put simply, it can be said that the Riksbank purchased bonds providing a fixed interest income, at the same time as the bonds are funded at a variable interest cost in the form of the policy rate. If the average policy rate until the bonds mature becomes higher than the fixed interest income from the bonds, the Riksbank’s negative net interest income will be negative and losses will arise.

With the accounting rules used by the Riksbank, the bond holdings are market-valued at the end of each year. Put simply, the market value means that the expected negative net interest income for the years ahead is already having an impact on the financial result.

The market value largely depends on what market participants believe about future interest rate developments. Over the past year, as the Riksbank started to raise its policy rate, market participants revised their expectations of future policy rates upwards. Long market rates rose and bond values fell. The market value of the bonds has thus become lower than the acquisition value. An unrealised loss has thus arisen on the Riksbank’s bond holdings.

The Riksbank is not alone in making large losses on its securities holdings due to the rising interest rates. Other central banks, such as the Reserve Bank of Australia (RBA), the Bank of England (BoE), the European Central Bank (ECB) and Federal Reserve (Fed), among others, have made similar purchases of securities and have communicated that they are making and/or are expected to make losses in the future.

Could you have done anything to avoid this large loss?

No, the securities purchases were based on well-informed decisions that the Executive Board of the Riksbank deemed necessary to mitigate negative consequences and major risks for the economy. Like several other central banks, the Riksbank initially purchased assets to make monetary policy more expansionary with the aim of achieving price stability in a situation with very low inflation and a policy rate that was almost zero, in principle. During the pandemic, the bond purchases were expanded to safeguard the supply of credit in the economy and contribute to the favourable development of the economy.

When inflation rose as the pandemic subsided and Russia invaded Ukraine, the Riksbank, like other central banks around the world, needed to tighten monetary policy to combat inflation. This led to rising interest rates both in Sweden and abroad.

Did the Riksbank’s portfolio of government bonds cause the Riksbank’s losses?

The loss made by the Riksbank in 2022 is linked to rising global interest rates, which has led to a fall in market values for interest-bearing securities around the world. The Riksbank holds both Swedish interest-bearing securities purchased for monetary policy reasons and foreign interest-bearing securities included in the foreign exchange reserves. Rising Swedish and foreign interest rates led to losses in both portfolios in 2022. However, partly because the holdings of Swedish securities are larger than those of foreign securities, they account for a larger part of the total loss. Of the total losses of SEK 81 billion in 2022, Swedish assets accounted for SEK 59 billion, while the loss on foreign assets amounted to SEK 37 billion. Losses on foreign assets were mitigated by realised foreign exchange gains of SEK 10 billion (read more about the Riksbank’s financial result for 2022 in the Riksbank’s Annual Report).

The bond losses have resulted in the Riksbank having negative equity. How long can the Riksbank function normally and conduct monetary policy in such a situation?

In the short term, losses from securities holdings do not affect the Riksbank’s ability to fulfil its tasks. The Riksbank can continue to conduct an effective monetary policy and operate in a normal manner. A central bank can always pay its way in its own currency by creating what is known as central bank money. Consequently, for a period, it can have negative equity and still perform its tasks. There are relevant examples of this, including the Czech National Bank (CNB) (see also Vredin and Nordström Staff memo).

In the longer term, an insufficient level of equity may lead to a deterioration in the central bank’s ability to finance its activities on its own. Ultimately, this could affect public confidence in the central bank’s ability to perform its tasks independently. A central bank such as the Riksbank thus needs a level of equity that can ensure its financial independence.

Is it common for the Riksbank to make a loss?

No, not so common, but from time to time the Riksbank has made small losses. Apart from the large loss in 2022, the Riksbank has reported negative results on three occasions since 2004 and, on these occasions, losses have been significantly lower than in 2022.

You say that the gains for society outweigh the losses you have made. Can you demonstrate this? What evidence do you have for it?

The Riksbank’s asset purchases were made in a strained situation internationally, when the larger central banks around the world were conducting very comprehensive securities purchases. The Riksbank purchased government bonds in the period 2015–2021 to maintain confidence in the inflation target, secure the credit supply during the coronavirus pandemic and contribute to the favourable development of the economy. International research and analyses made by staff members at the Riksbank show that securities purchases contribute to lower interest rates, more expansionary financial conditions, higher economic activity and lower unemployment, which in turn strengthens public finances. The financial and economic effects of asset purchases can be estimated in different ways, for example by using macroeconomic models, and by studying what happens on financial markets when central banks announce asset purchases.

An Economic Commentary by Riksbank staff members Kjellberg and Åhl uses the effects of such a macroeconomic model as a starting point. According to the simple calculations included in the Commentary, asset purchases have strengthened public finances by an amount in the order of SEK 40 billion and have helped lower interest costs by about SEK 30 billion. This Economic Commentary makes several references to Swedish and international studies in the field.

What happens when the Riksbank makes a profit or a loss?

When the Riksbank’s reported result is positive, that is when the Riksbank makes a profit and equity is above the target level, the profit is paid to the state. However, the Riksbank can use profits to make what are known as financial risk provisions and thus build up capital buffers to cover any future losses. For 2022, for example, the Riksbank reversed earlier risk provisions to reduce the reported loss. This century, the Riksbank has made profits to the extent that it has distributed SEK 156 billion to the state in total. This is almost twice as much as the loss the Riksbank made for 2022, which was SEK 81 billion.

When the Riksbank’s reported results are negative, that is when the Riksbank makes a loss, the Riksbank’s equity decreases by a corresponding amount. In such cases, there is no distribution of profits to the state. Decisions on the allocation of profit, that is, how any gains or losses are to be distributed, are taken by the General Council of the Riksbank. After that, the decision of the General Council needs to be approved by the Riksdag, the Swedish parliament. How this is to be done and how the distribution of profits is to be calculated are regulated in the Sveriges Riksbank Act (read more about profit distribution in chapter 8 of the Sveriges Riksbank Act). This also stipulates how much equity the Riksbank should have.

About the Riksbank’s accounting policies

What is the difference between a balance sheet and a profit and loss account?

The balance sheet presents the value of the Riksbank’s assets and liabilities.

The assets show what the Riksbank owns and the liabilities show how the assets are financed.

This means that the total value of the assets must always correspond to the total value of the liabilities, meaning that the assets and liabilities must be in balance.

The liabilities are divided into liabilities to the owner (the Riksdag) and liabilities to parties other than the owner. The liabilities to the owner are recorded in the Riksbank’s balance sheet under the items Revaluation account, Equity and Result for the year.

The item Result for the year corresponds to the sum of all revenue and expenses recognised in the profit and loss account.

Why do central banks use so-called revaluation accounts?

Unrealised gains on the Riksbank’s assets are recorded in so-called revaluation accounts. The purpose of these accounts is to make it easier for central banks to avoid distributing unrealised gains to the Treasury. The value of the Riksbank’s assets can vary considerably over time.

Distributing unrealised gains to the government could erode the central bank’s assets.

However, the extent to which unrealised gains should be distributed is ultimately decided by the General Council of the Riksbank and the Riksdag.

Must the Riksbank value its bond holdings at market value?

The Riksbank values both the foreign bond holdings in the foreign currency reserves and the bond holdings in Swedish kronor at market value.

According to the accounting rules, the Riksbank must report the foreign bond holdings at market value but has the possibility, based on monetary policy considerations, to value the bond holdings in Swedish kronor held for monetary policy purposes at accrued acquisition value.

The difference between these two valuation principles is that the market value corresponds to the sum of the bond’s future cash flows discounted at the current market rate and the accrued acquisition value corresponds to the sum of future cash flows discounted at the market rate when the bond was acquired. Both principles give the same total result if the Riksbank holds the bonds until maturity.

When measured at accrued acquisition value, the result tends to be more evenly distributed over the holding period, provided that the bonds are held to maturity.

The Riksbank has chosen to use the same valuation principle consistently for all assets, and thus be transparent about what losses (or gains) are expected in the future, and to demonstrate the consequences of selling the holdings before they mature.

In addition, the valuation principle the Riksbank has chosen for the monetary policy bond holdings is in line with the international accounting policies stated in IFRS 9, where financial assets are to be valued at market value, also known as fair value, if the assets may be subject to sale before they mature. The Riksbank has not promised that the assets will be held to maturity and, at the beginning of April 2023, the sale of parts of the monetary policy bond holdings began.

What does it mean when unrealised losses are transferred to the profit and loss account?

When market value is lower than acquisition value, an unrealised loss arises and is recorded in the profit and loss account at year-end as a write-down.

At the same time, the acquisition value is adjusted downwards to the current market value. This means that future market rates for gold and each individual foreign currency holding in the foreign exchange reserves will be compared with this adjusted acquisition value when future unrealised gains and losses are calculated. For individual bond holdings, the amount written down as a result of a decline in the market price of the bond will then be reversed in the profit and loss account as the decline in value does not affect the fact that the nominal amount of the bond is expected to be repaid at maturity. This takes the form of increased interest income until the bond matures or is sold, thus generating a profit.

Who decides on the appropriation of the Riksbank’s profits?

The Riksbank is a public authority accountable to the Riksdag. Under the new Sveriges Riksbank Act, the General Council of the Riksbank decides on the appropriation of the result for the year and the Riksdag approves the General Council’s decision. This arrangement applies from the start of the financial year 2023.

Thanks for your feedback!

Your comment could not be sent, please try again later

Questions? Visit our FAQ on kundo.se (opens i new window).