Q&A - The Riksbank's income statement and balance sheet

The Riksbank asked for a capital injection of 44 billion but you are only receiving 25 billion, are you happy with that?

This spring the Riksbank made a submission to the Riksdag to restore the bank's equity to the statutory base level. This meant a capital injection of SEK 43.7 billion. As an alternative, we proposed to split the restoration over two years, with 25 billion in a first step. The capital injection of SEK 25 billion now decided by the Riksdag means that our equity (which at the end of 2023/beginning of 2024 was SEK -2 billion) amounts to SEK 23 billion before the result for 2024 is taken into account.

In connection with the decision on the capital injection, the Riksdag stated that it is important that the Riksbank has adequate self-financing capacity. The Ministry of Finance has drafted a bill which, among other things, proposes that the Riksbank can request interest-free deposits from the credit institutions. As the Riksbank writes in its consultation response, the requirement for interest-free deposits means that the Riksbank will have better -financing capacity, which we are in favour of.

When can the Riksbank start paying out dividends to the state again?

It will take a long time for the Riksbank to build up equity to the target level that will enable dividends to be distributed again (see, for example, the baseline scenario presented by the Riksbank in the annex to its consultation response).

Will the proposal in the bill on interest-free deposits contribute to better earnings for the Riksbank?

The bill proposes that the Riksbank will be able to require interest-free deposits from credit institutions. The size of the interest-free deposits will be determined by the difference between the level of equity and the target level for equity. The deposit requirement means that the Riksbank can have interest-free funding of its assets in a situation where equity (which is also interest-free) is low. In this way, the interest-free deposits improve the Riksbank's net interest income, which is the basis for the Riksbank to be self-financed.

Why does the Riksbank need better earnings?

The Riksbank's financial independence entails the Riksbank being able to finance its own operating costs, independently and in the long term. Financial independence is achieved primarily through the Riksbank’s net interest income, that is, the difference between interest income and interest expenses, covering operating costs and creating scope for financial risk provisions. The Riksbank can achieve positive net interest income by having access to interest-free debt, meaning sources of funding on which the bank does not pay interest. This includes equity and currency in circulation. The demand for currency has been shrinking for a long period of time and the Ministry of Finance's proposal for a requirement for interest-free deposits means that the Riksbank will have access to another type of interest-free debt that can contribute to the Riksbank improving its self-funding.

How can the Riksbank rebuild its equity?

Today, there are in principle two ways in which the Riksbank can rebuild its equity: by making profits or by receiving a capital injection. The Ministry of Finance's proposal for a requirement for interest-free deposits from credit institutions will improve the Riksbank's earning potential and enable the Riksbank to build up equity at a slightly faster pace than we can today.

What is the difference between interest-free deposits and a reserve requirement?

A reserve requirement is primarily a monetary policy tool or, as in some countries, a financial stability tool. A reserve requirement is mainly used to manage liquidity in the financial system and need not be interest-free. The interest-free deposit requirement is similar to a reserve requirement, as both require credit institutions to hold deposits with the central bank, but the purpose of the deposit requirement is different.

You said earlier that you would investigate long-term earnings. What happened to that investigation? What alternative sources of income are available?

The Riksbank's self-sufficiency depends on both costs and income. We aim to reduce our costs while exploring ways to increase revenues in areas such as foreign reserve management. If the Riksbank can impose a requirement for interest-free deposits, it will also help to strengthen long-term earnings.

How much do you expect to raise through the interest-free deposit requirement?

Earnings will vary depending on the size of the Riksbank's equity, the target level of equity and the policy rate. It is therefore difficult to say what interest-free deposits might generate once they are implemented. Assuming that the Riksbank can withdraw interest-free deposits equivalent to around SEK 40 billion and the policy rate is 3.5 per cent, this would mean a cost saving of SEK 1.4 billion in one year. (Read more about earnings from the interest free deposit requirement in the annex to the Riksbank´s consultation response.)

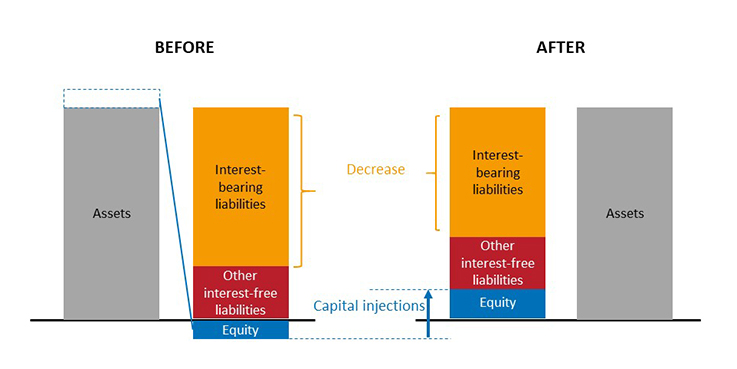

What happens on the Riksbank’s balance sheet when the bank receives a capital injection?

The size of the Riksbank's balance sheet will remain unchanged, but there will be a change between the various items on the liabilities side of the balance sheet. This is because the monetary policy deposits (the banks’ overall claim on the Riksbank) decreases, while the Riksbank’s equity increases to the same extent.

The state transfers funds to the Riksbank by transferring money to the Riksbank in the RIX system. This type of transaction means that the total amount of central bank reserves in the system decreases, which is the same as a reduction in monetary policy deposits. The Riksbank transfers the payment to the primary capital fund on the Riksbank's balance sheet. The primary capital fund, together with the reserve fund and retained profits, constitutes the Riksbank's equity.

On the Riksbank’s balance sheet, shown in simplified form in the figure below, this becomes visible when equity grows and shifts from negative to positive at the same time as monetary policy (interest-bearing) deposits shrinks. Overall, the size of the balance sheet does not change but there is a redistribution between interest-bearing monetary policy deposits and interest-free debt, equity.

What happens when the Riksbank makes a profit or a loss?

When the Riksbank's reported result is positive, i.e. when the Riksbank makes a profit, and equity is below the target level for equity, profits are used to build up equity. When equity is at the target level, any profits will be distributed as dividends to the state. However, the Riksbank can use all or some of the profits to make what are known as financial risk provisions and thus build up buffers to cover any future losses.

This century, the Riksbank has made profits to the extent that it has distributed dividends of a total of SEK 156 billion to the state. This is almost twice as much as the loss the Riksbank made for 2022, which amounted to SEK 81 billion.

When the Riksbank’s reported results are negative, that is when the Riksbank makes a loss, the Riksbank’s equity decreases by a corresponding amount.

It is the General Council of the Riksbank who decides on the appropriation of profit, that is, how any gains or losses are to be distributed. After that, the decision of the General Council needs to be approved by the Riksdag, the Swedish parliament. This process is regulated in the Sveriges Riksbank Act (read more about profit distribution in chapter 8 of the Sveriges Riksbank Act).

Why can the Riksbank not ensure financial independence by using the seigniorage from cash supply?

In most other countries currency in circulation is both large and growing this allows interest-free capital to generate sufficient returns even if equity decreases. In Sweden however, the amount, of currency in circulation is small and has decreased as a proportion of GDP in recent decades due to a reduced demand for cash (read more about cash and payments in the Payments Report). Currency in circulation has also fallen as a proportion of the balance sheet, resulting in seigniorage having made an increasingly smaller contribution to the Riksbank’s financial result over a long period of time. This means that the Riksbank, unlike other central banks that have made large losses, has greater difficulty in restoring its equity under its own steam by means of a large seigniorage.

What is the difference between a balance sheet and a profit and loss account?

The balance sheet presents the value of the Riksbank’s assets and liabilities.

The assets show what the Riksbank owns and the liabilities show how these assets have been financed. This means that the total value of the assets must always correspond to the total value of the liabilities, meaning that the assets and liabilities must be in balance.

The liabilities are divided into liabilities to the owner (the Riksdag) and liabilities to parties other than the owner. The liabilities to the owner are recorded in the Riksbank’s balance sheet under the items Revaluation account, Equity and Result for the year.

The item Result for the year corresponds to the sum of all revenue and expenses recognised in the profit and loss account.

Why do central banks use so-called revaluation accounts?

Unrealised gains on the Riksbank’s assets are recorded in so-called revaluation accounts. The purpose of these accounts is to make it easier for central banks to avoid distributing unrealised gains as dividends to the state. The value of the Riksbank’s assets can vary considerably over time.

Distributing unrealised gains to the government could erode the central bank’s assets. However, the extent to which unrealised gains should be distributed as dividends is, in Sweden, ultimately decided by the General Council of the Riksbank and the Riksdag.

Must the Riksbank value its bond holdings at market value?

The Riksbank values both the foreign bond holdings in the foreign currency reserves and the bond holdings in Swedish kronor at market value.

According to the accounting rules, the Riksbank must report the foreign bond holdings at market value but has the possibility, based on monetary policy considerations, to value the bond holdings in Swedish kronor held for monetary policy purposes at accrued acquisition value.

The difference between these two valuation principles is that the market value corresponds to the sum of the bond’s future cash flows discounted at the current market rate and the accrued acquisition value corresponds to the sum of future cash flows discounted at the market rate when the bond was acquired. Both principles give the same total result if the Riksbank holds the bonds until maturity.

When measured at accrued acquisition value, the result tends to be more evenly distributed over the holding period, provided that the bonds are held to maturity.

The Riksbank has chosen to use the same valuation principle consistently for all assets, and thus be transparent about what losses (or gains) are expected in the future, and to demonstrate the consequences of selling the holdings before they mature.

In addition, the valuation principle the Riksbank has chosen for the monetary policy bond holdings is in line with the international accounting policies stated in IFRS 9, where financial assets are to be valued at market value, also known as fair value, if the assets may be subject to sale before they mature. The Riksbank has not promised that the assets will be held to maturity and, and at the beginning of April 2023, the sale of parts of the monetary policy bond holdings began.

What does it mean when unrealised losses are transferred to the profit and loss account?

When the market value is lower than the acquisition value, an unrealised loss arises and is recorded in the profit and loss account at year-end as a write-down. At the same time, the acquisition value is adjusted downwards to the current market value. This means that future market rates for gold and each individual foreign currency holding in the foreign exchange reserves will be compared with this adjusted acquisition value when future unrealised gains and losses are calculated. For individual bond holdings, the amount written down as a result of a decline in the market price of the bond will then be reversed in the profit and loss account as the decline in value does not affect the fact that the nominal amount of the bond is expected to be repaid at maturity. This takes the form of increased interest income until the bond matures or is sold, thus generating a profit.

Who decides on the appropriation of the Riksbank’s profits?

The Riksbank is a public authority accountable to the Riksdag, the Swedish parliament. Pursuant to the Sveriges Riksbank Act, the General Council of the Riksbank decides on the appropriation of the result for the year and the Riksdag approves the General Council’s decision. This arrangement applies from the start of the financial year 2023.

Thanks for your feedback!

Your comment could not be sent, please try again later

Questions? Visit our FAQ on kundo.se (opens i new window).