Scenario for results and capital

Published: 4 July 2022

The Riksbank's financial results, and ultimately its equity, are thus affected by the composition of the balance sheet and the pricing of interest rates and exchange rates on the market. It is important to understand how the results and capital may develop in the future, both to be able to make forecasts of the dividends to the treasury and to be able to accurately assess the financial risk picture and the amount of capital that may need to be allocated as a buffer; so-called financial risk provisions.[16] See Sveriges riksbank (2021a) and Sveriges riksbank (2022d). The Riksbank regularly calculates various scenarios and simulations of how the balance sheet may develop. Below we review one of these scenarios, which illustrates what happens if the current rise in market rates continues.

Assumptions for the scenario

In a scenario for the Riksbank's reported results and capital, we need to assume something about how the Riksbank chooses to change its balance sheet and how financial prices develop going forward. We assume that the bond holdings in Swedish kronor follow the monetary policy decision in April during the rest of 2022 and that no further purchases are made thereafter, which means that the holdings gradually shrink as they mature.[17] This corresponds to the lower limit of the inner interval in Figure 8 in Sveriges riksbank (2022a, s. 14). The chart does not extend over the entire period of our scenario, but the same assumption applies beyond the chart’s horizon. This should not be seen as the Riksbank's official view of the future holdings but as a technical assumption. Note that the decision regarding asset purchases for the remainder of 2022 from the latest monetary policy meeting, in June, has not been taken into account in this scenario. This means that the interest-bearing debt will also gradually fall, as the banks' deposits in the Riksbank decrease to the same degree.

For financial prices, i.e. interest rates and exchange rates, our assumptions in this scenario are largely based on market pricing in mid-May, see Figures 6-8 in the Appendix.[18] In some cases, reliable market pricing is not available far into the future. In these cases, we have made simple and arbitrary assumptions beyond the horizon where market pricing is applied. In the scenario, bond rates in both Sweden and the rest of the world will therefore rise, as central banks are expected to raise their policy rates sharply in the coming years. For example, we assume that the Riksbank's policy rate will rise, in accordance with what forward rates were in mid-May, and reach its highest listing of about 2.5 per cent in 2024, and then fall gradually to just over 2 per cent.[19] Since mid-May, the market pricing of the future Riksbank's policy rate has risen further. Further details of the assumptions are described in the Appendix.

The Riksbank's results and capital according to the scenario

The assumptions presented above give an estimated development for the Riksbank's financial results going forward. The results in turn affect equity.

The Riksbank is expected to make a major loss in 2022

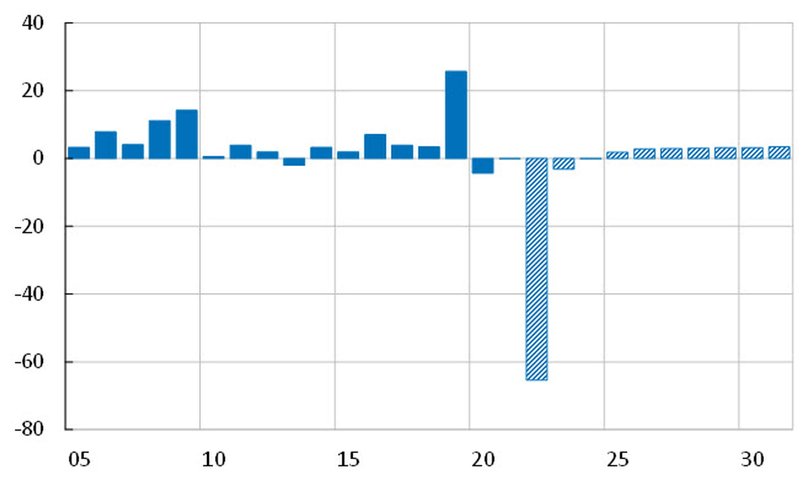

In the scenario, market rates in both Sweden and the rest of the world rise rapidly during 2022. This means that the market value of the bonds in both the foreign exchange reserves and the Swedish portfolio will fall rapidly during the year, which in turn leads to a severely negative result this year, SEK -65 billion, see Figure 4.[20] Note that the scenario is very uncertain and that we do not know what this year’s result will be until after the turn of the year.

At the same time, the purchase value of large parts of the bond holdings is written down at year-end. This means that higher interest income is recorded during the remaining duration of the bonds. When the policy rate is raised, the Riksbank's interest expenses on deposits in SEK rise, but this is offset by the higher interest income.[21] An alternative way of describing this is that the higher interest income from write-downs offsets the Riksbank's reported loss, while the rising interest expenses affect the reported results. The results are therefore close to zero or slightly positive during the remaining years.

Note. Broken bars represent the scenario.

Source: The Riksbank

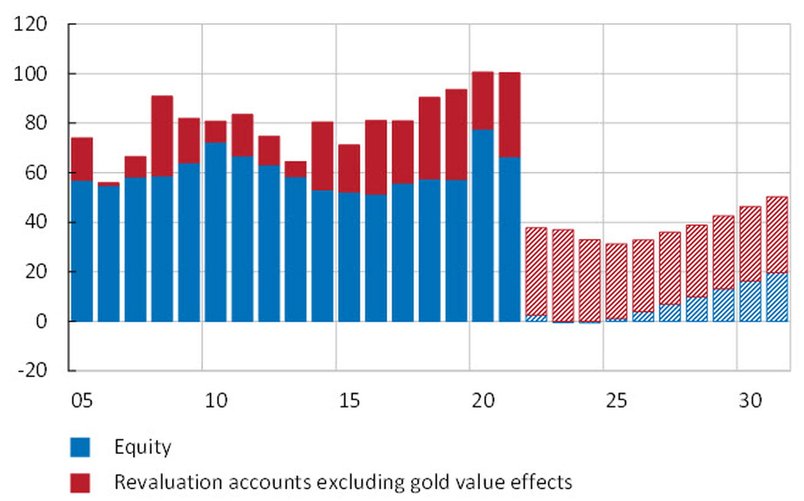

Equity falls to about zero

For a long period, the Riksbank has had a reported equity of between SEK 50 and SEK 80 billion, see Figure 5. In the scenario, the large loss hits equity, which falls to a level around zero. Although the results turn positive a few years ahead in the scenario, it takes more than a decade for the Riksbank to rebuild its equity with its own profits.

If we assume that the proposal for a new Sveriges Riksbank Act takes effect from the 2023 accounting year, the rules for profit dividends from the Riksbank to the treasury will change (see the article). In this scenario, there is no scope for such dividends during the current period.[22] Even with the dividend principle used in the current Sveriges Riksbank Act, it can be expected that dividends will not be available for most of the scenario. Instead, it may be appropriate to apply the new act's rule on recapitalisation from the State to the Riksbank (see the special article).

ARTICLE – the Riksdag votes on the proposal for a new Sveriges Riksbank Act

On 1 June 2022, the Riksdag voted in favour of the first step of two towards adopting a new Sveriges Riksbank Act (Proposition 20121/22:41 and Report 2021/22:KU15).[23] See Sveriges riksdag (2022). The Riksdag will vote a second time after the autumn parliamentary elections, and if the draft law is approved, the new Sveriges Riksbank Act will enter into force on 1 January 2023.

The new act amends the rules for the Riksbank's dividends to the State and for equity. In brief, they mean that there is a target level for equity. This is set at SEK 60 billion as of 1 January 2023 and is subsequently adjusted upwards with CPI inflation each year. If the Riksbank makes a profit that results in equity exceeding the target level, the surplus part of the profit is distributed to the State. If, on the other hand, the Riksbank's equity falls below 1/3 of the target level, the Riksbank shall petition to the Riksdag for a recapitalisation. The amount requested shall normally bring equity up to the so-called basic level, which is 2/3 of the target level. However, if the Riksbank considers it necessary for it to have sufficient earning capacity and be self-sufficient in the long term, capital may need to be raised all the way up to the target level. However, the draft law says that the funds in the revaluation accounts should also be taken into account when determining the size of the capital injection required.

Figure 5 shows that in the assumed scenario the Riksbank's equity falls below 1/3 of the target level, and in this situation the Riksbank would therefore need to make a request for recapitalisation if the new Sveriges Riksbank Act had entered into force. However, if funds in relevant revaluation accounts are included, capital will be close to the basic level.[24] The Riksbank's gold reserve has a separate revaluation account which it is not appropriate to include because the gold does not mature and the Riksbank has no plans to sell it. Since the gold revaluation account is only a buffer against gold price losses in accounting terms, it is not, for example, a buffer against the type of interest-related losses that we mainly focus on here. This makes it difficult to assess what amount, if any, would be relevant for a racapitalisation request. We have therefore ignored the possibility of recapitalisation in the calculation of the scenario and simply note that this rule would be relevant in the new act in such a scenario.